Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

Google released their second quarter numbers post the bell yesterday, they were very good, in my opinion. You can download the .pdf: Google Inc. Announces Second Quarter 2014 Results and Management Change. Revenues for the quarter of 16 billion Dollars (an increase of 22 percent), operating income was 4.26 billion Dollars, 27 percent of revenues. Nice. On a non GAAP EPS, excluding stock-based compensation (SBC) expense (what the hell?) that number was 6.08 Dollars.

This is still an out and out advertising business. The volumes, or number of paid clicks increased 25 percent in the second quarter, 2 percent over the prior quarter. The cost per click, or the price that Google gets decreased 6 percent over the first quarter this year and 7 percent over the comparative quarter last year. Traffic Acquisition costs, or the money that is paid to the Google partners (advertising sharing) was nearly ten percent higher when compared to the corresponding quarter.

Cash on hand? A whopping 61.2 billion Dollars, they generated nearly three billion Dollars of cash in the quarter. As a percentage of the 395.7 billion Dollar market cap, that is 15.4 percent. Of course Google still does not pay a dividend. As they are a growth company (they hired around 2200 people over the quarter), meaning that costs are not exactly front and centre. They spent more on R&D, 14 percent of revenues, than JNJ, who spend just a little less than 12 percent. Astonishing how they encourage their workforce to express themselves, to find the next big thing. It is still just an online advertising business, that is it.

I think that this is one of the most fabulous investments that you can make, of course not for income and it certainly on a forward basis (modelling around 21 and half Dollars earnings) means that the company trades forward on 27 times earnings, this year. No dividend, quite expensive. And a year further forward, because earnings are expected to grow faster over the next two years. Quite quickly the forward multiple reduces to a 22, earnings for 2015 as per the analyst community are expected to be over 27 Dollars for the year.

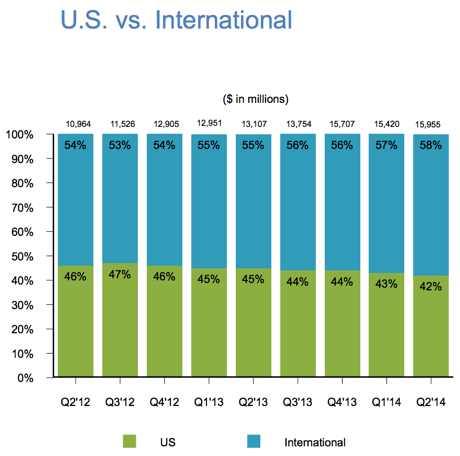

This businesses revenue mix has also changed, it is now less of a US business and more of an international business, as per the graphic from the presentation slides:

Almost a percent per quarter shift, as a shareholder you want more geographies, more languages, more businesses and more customers from all around the world. The internet of things, in which everyone will be connected will of course have many advertising platforms, from your fridge, to your car, to buildings, to everything in-between. Fibre, that is going to be big, the company is certainly teeing up for all their other businesses. Apps, content in the "store", that is set to become bigger, there are hundreds of Android users out there looking for apps. We continue to add to what is an amazing business now and what I consider the General Electric of the 21st century and a must own.