Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

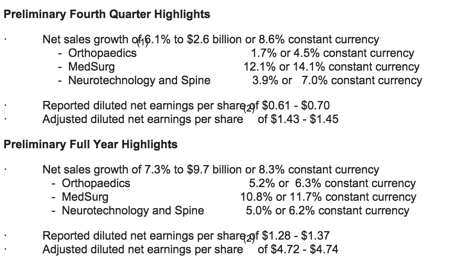

Yesterday we received 4th quarter and full year results from one of our recommend healthcare stocks in the US namely Stryker. I've taken a screen grab from the presentation which summarises sales growth amongst the business's divisions. MedSurg is the devices and equipment division, the other 2 are self explanatory.

As you can see, the growth has been solid. The US which is responsible for 68% of sales saw sales growth of 9.6% for the year while their international sales which represent 32% saw an increase of 2.6%. Notice a pattern there? Yes the US economy is outperforming everyone else but don't forget that the US companies who manufacture locally and export their goods are getting hit hard by the ever strengthening dollar. I guess that is a function of a growing US economy which is still Stryker's main market. I'd say an overall net positive macro environment for the company. A much better scenario than having a weaker dollar due to a weaker US economy.

The company made $4.74 for the year which trading at $94 gives it a historic PE of 19.8. Forecasts are for $5.17 for 2015 putting the business on a forward multiple of 18 which is not bad for a company with a strong balance sheet, operating in an exciting sector.

The company is certainly in acquisitive mode. The sector is fragmented and we saw lots of M&A activity throughout 2014. Stryker's most recent activities include a strategic partnership with a stem cell company called Osiris to develop bone matrix tissue and special wound repairing technologies. Sounds exciting! Another deal was to acquire assets in a Canadian hospital beds manufacturer. Talk of other big deals are always floating around.

In the US healthcare has been thriving. The healthcare index was up 22.3% last year. Stryker is a big benefactor if the industry is spending. If hospitals are making good money and increasing their capex spend then the devices businesses will be benefiting. In this fast growing environment Stryker are stealing market share, growing organically and sit with plenty of growth via acquisition opportunities.

Developed markets are riddled with old and overweight people. They will be Stryker clients. So will the fitness freak who has run his hundredth marathon. The company sits in a sweet spot and we continue to accumulate.