Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

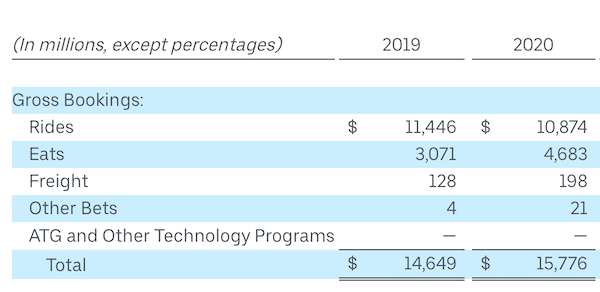

Last week Uber released their Q1 results. For very obvious reasons, this is a company heavily impacted by a pandemic. Bookings for the quarter came in at $15.8bn, ahead of expectations of $15.7bn. This was because of a massive increase in Uber Eats (up 54%) while rides declined 3%. Here is the breakdown of their quarter.

Monthly Average Users increased 11% to 103 million. Margins increased as they left eight unprofitable markets for Eats. Fortunately, South Africa was not one of those markets.

Rides in April (this current quarter) dropped 80%. Ouch! But in the first week of May rides globally picked up 12%.

We see this period as an opportunity to streamline its business (close non-profitable markets) and expand on its Eats business where they are doing well. Mobility will be impacted for a while to come but keeping vehicle's sterilised and screening drivers is manageable. A lot more than the airlines. Besides, people may prefer an Uber ride to a train or a bus?

Alternatives like their scooter rental business, which keeps the rider separate from others and outdoors, should also thrive. They recently merged their scooter business with Lime whilst adding a further $170m to the venture. Speaking of cash, they are sitting on $11bn in cash, which they deem more than enough to weather this storm.

It won't be a smooth ride but we see Uber as a good recovery bet.