Market Scorecard

Markets are buoyant at the moment, with Asian markets having their best day since January. Positive retail sales out of the US, further assurances from Jerome Powell around keeping interest rates low and analyst upgrades to Apple, all playing their part. Not even Boeing's 5% drop yesterday could keep the market down.

Then a late night clarification from the EU and UK, around sticking points in their current deal were announced, where essentially Europe is committing to negotiate in good faith to find solutions to the current backstop. The new commitments from the EU are expected to help Theresa May get more votes in the UK parliament tonight. Political analysts that I am reading still think she will fall short of the required votes though, but that the defeat won't be as bad as a few weeks ago. This is progress of some sort.

Yesterday the

JSE All-share closed up 0.17%, the

S&P 500 closed up 1.47%, and the

Nasdaq closed up 2.02%.

Company Corner

Bright's Banter

Africa's pharmaceutical giant Aspen, reported very soft interim numbers on Thursday night, sending the share price down as much as 50% intra-day on Friday. The stock eventually closed down 29%, at the lowest levels in seven years. The main concerns were mounting debt on the balance sheet and the delayed sale of the infant nutrition business.

The Umhlanga-based group said that revenues for the half-year were up 1% to R19.7 billion, but earnings were down 9% to R3.6 billion. That's

not good enough for a company that's expected to grow earnings by double digits. Net debt grew by R6.7 billion to R53.5 billion in the period due to deferred acquisition payments of R4.9 billion and capex of R1.5 billion.

Aspen was built deal-by-deal, starting from the year 1999 when Steven Saad and Gus Attridge bought SA Druggists out of liquidation, with the help of a big loan from Investec. They soon dominated pharmaceutical markets in South Africa and then started branching out offshore. The company was the first in Africa to produce generic ARVs in 2003, and a year later went after the infant nutritional formula business. Stephen Saad is an accountant and loves deals, so the group did an array of dazzling acquisitions, mostly of older drugs and manufacturing facilities from global groups like GlaxoSmithKline, Merck and AstraZeneca.

They are now a fair sized global player in anaesthetics and thrombosis (anti blood-clotting) drugs. They have sales teams in 56 countries, and 25 manufacturing sites around the world.

During the 15 year period after its JSE listing, the share price flew from R4 to an all-time high of R438. Early signs that some of their acquisitions were battling and an exit by an anchor shareholder led to a cooling down to the R250-R300 range. Note that the group has never done an equity raise from shareholders. They accessed debt in European capital markets, which readily advanced them the R53.5 billion debt pile they are saddled with today.

The problem is that despite heavy restructuring, not all of these businesses are as cash generative as expected. To pay down the debt, some assets need to be sold. This may put them in a weak position, where crown jewels will be sold first as those are easy to sell. It's not easy to command good prices when you are a forced seller. On the other hand, Saad argues that these debt levels have peaked, and that second half cash flows will be stronger.

On the 14th of September, Paul wrote that Aspen was selling its infant formula business to French milk produced Lactalis for $865 million (about R13 billion at the time). This deal was going to help Aspen raise the necessary cash to ease the debt burden but the deal is still subject to final regulatory approval in New Zealand. If that approval is not forthcoming, there's cause for concern. If it closes at the end of May as hoped, a net amount R10.4 billion will be banked.

As an aside, I (Bright here) worked in this industry as a management trainee before joining Vestact. Infant formula went from being sold on the aisles by retailers to being pushed to the back where they're locked up like cigarettes due to regulatory reasons. Manufacturers of infant formula aren't allowed to market to mothers and mothers to be, and only a healthcare professional (dieticians mostly) can talk about such things.

If any infant formula factory faults are discovered, the whole batch needs to be destroyed by qualified professionals at a very high cost. The manufacturing process is monitored by onerous ISO regulations to ensure good quality. Every single step eats away into the margins slowly until the fat margins are super thin. This business is mostly a volume driver! I'm actually quite relieved it's being sold.

According to market sources, the biggest reason for Aspen's share price swoon is a suspicion that the company might need to raise more capital via a rights issue, to drum up anywhere between R10 billion and R20 billion in order to be able to pay down a EUR 1 billion loan that matures in May 2020 and the EUR 500 million facility due in May 2020.

Stephen Saad has made it quite clear, that the only thing that's keeping him up at night is the debt level which now exceed the market capitalisation. He says that he will do whatever it takes to bring them back down to respectable levels before pursuing "niche opportunities".

We are still strong supporters of Aspen. We first invested in them at R20 a share. They are tough and talented operators. Once again, the stock seems oversold. We thought it was cheap at R230 in September 2018 and now it's at R102.50 which hurts like hell. We will hang in there.

Our 10c Worth

One thing, from Paul

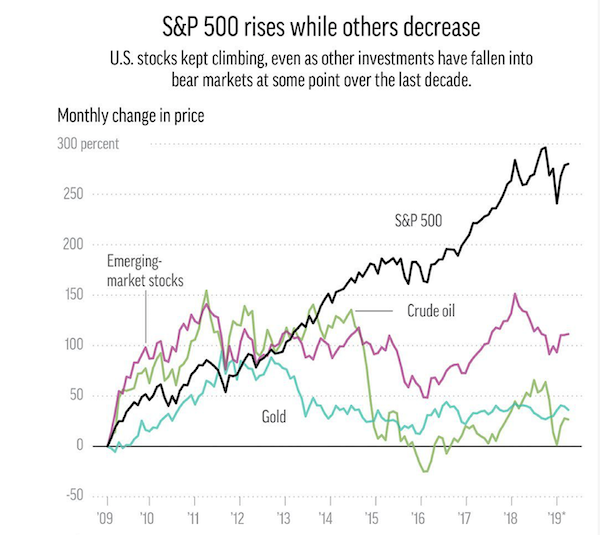

Here's a chart that

shows how well US stocks (the S&P 500) have performed over the past decade, compared to some other well-known asset classes. As you know, 9 March 2009 was a low point in markets, after the sub-prime mortgage crisis in 2008.

Emerging market equities have also been good, but have not done as well. Crude oil and gold have sucked.

Michael's Musings

Over the weekend Tesla announced that they will close fewer stores than originally planned. They will do that buy raising their car prices by 3%, all except the $35 000 version -

Tesla will raise prices on its cars, reverses plan to close stores

Other news from the company, is that

they have secured funding for their new factory in China. Based on the below graph, it is clear how important the Chinese market will be for Tesla. Note the percentage of electric car sales in Norway, interesting.

You will find more infographics at

Statista

Linkfest, Lap it Up

Amazing. Imagine the camera equipment used to capture these -

These Groundbreaking Images Of A Sonic Boom Are Stunning

As many people who have moved from Jo'burg to Cape Town have discovered

As many people who have moved from Jo'burg to Cape Town have discovered, property prices in Cape Town are expensive. Compared to global prices, it still looks like value for money though.

You will find more infographics at

Statista

Vestact Out and About

Signing off

Signing off

Our market is soaring higher today, along with the rest of the globe. Key data out today is UK GDP, US CPI and then the big Brexit vote from the UK Parliament tonight.

Sent to you by Team Vestact.