Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

Last week, before all the public holidays, Facebook released their first quarter numbers which are their first since the data sharing scandal broke. These numbers only contain 2-weeks of post-scandal data; we will have to wait another quarter to see if there was any significant fallout from the scandal. Having a look at their numbers and reading the earnings call with investors afterwards, there was very little impact on user numbers. The bigger impact will be seen in costs associated with making data more secure, and having more stringent requirements for advertisers.

On to their very impressive numbers for the quarter. Revenue was up 49% to $11.97 billion, and costs for that revenue only up 39%, meaning their operating margin increased from 41% to 46%. A major contributor to the cost increase was a big step up in headcount, an increase of 48% to 27 700 employees. The increased revenue and increased margins meant that their net income was up 63% to $5 billion for the quarter. Year over year, they grew their user base by 13% to 1.45 billion daily active users and 2.2 billion monthly active users.

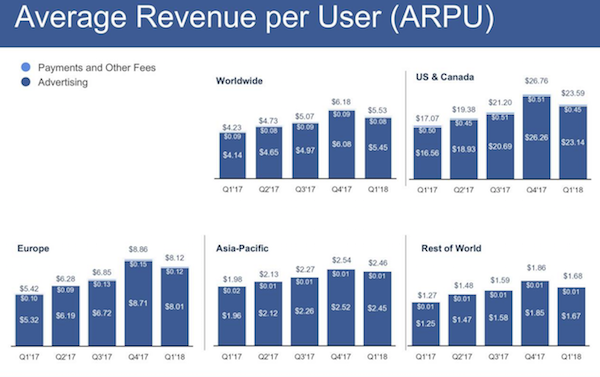

Given that Facebook is an advertising company, we have to ask if they have been able to make their user-base more profitable; yes they have. The graph below shows how much potential there still is outside of North America.

Going forward, a combination of a self-imposed increase in data security and the soon to be implemented EU GDPR (General Data Protection Regulation) is forecast to be a headwind to their top line growth. The company says that they are optimistic that the impacts will be muted, but they just don't know what the industry-wide ripples from GDPR will be.

For investors, the company is planning on spending more of their $44 billion cash pile on share buy-backs, increasing it from the current $6 billion plan to a new $15 billion plan. If you think that Facebook is still going to be relevant in 5-years, then the company will go from strength to strength. They have yet to monetise WhatsApp, they are taking things slowly with Facebook Messenger and Oculus is in it's infancy (You Can Now Buy Facebook's Phone-Free Oculus Go VR Headset).