Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

On Monday there were Full Year numbers from Discovery, which didn't disappoint. The results are broadcast on TV, making it easy to watch and pause if need be. Adrian Gore's passion for the business sure is inspiring. Recent books that I have read all talk about the importance of the vision from a founder. Founders generally have more credibility and business-wide support, meaning they can push companies in directions that professional managers would struggle. Adrian Gore and Stephen Saad are the first two South African leaders that come to mind when I think of inspirational leaders. But we are blessed with many.

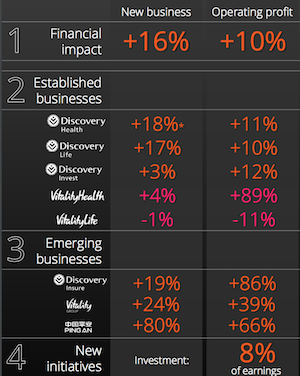

Here is a quick look at the group's performance as a whole.

The numbers in pink are their UK operations, which have been hit hard by Brexit. The group estimate's that Brexit has had at 25% impact on the profit for the Vitality Life business, ouch! Looking at the other UK business, Vitality Health, that huge jump in profit is due to the previous period having some once-off costs, so it was coming off a low base. Both UK divisions aren't doing as well as management had previously hoped but are moving in the right direction. Vitality UK is a superior product to traditional medical aid and life insurance. Their marketing is all over the place, you can't watch UK sport now without seeing Vitality branding somewhere.

The human behaviour data they have acquired, unsurprisingly is being put to good use in the UK. When people sign up for the Apple Watch incentive program, they saw a 42% increase in physical activity. From Discovery's perspective that is money well spent.

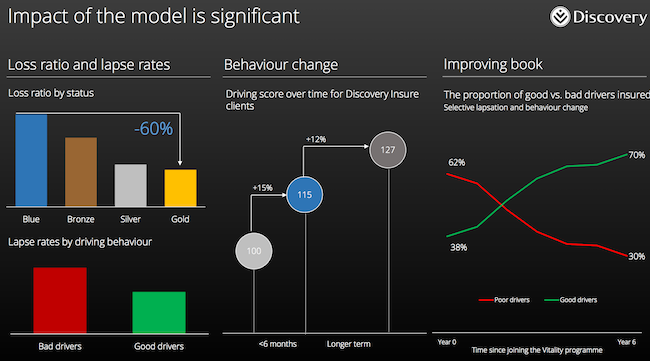

The Discovery Insure division has clear benefits from the incentives program. The division is still relatively new and falls in the group's 'emerging businesses' segment. Discovery Insure only started making money in the second half of the year and was loss-making for the full year. For 2018 though we should see a nice juicy profit. Their focus on driving quality, has resulted in new customers improving their driving by 27% in the first year on average. Even better, bad drivers are more likely to move to other insurers, meaning they are left with a higher proportion of their book in good drivers.

A bit of shameless Discovery promoting, I am an Insure customer. Since joining, I am more aware of my driving and for my efforts, I get over R1k back a month. The only problem now is that my wife's driving score is substantially higher than mine; I get reminded of that fact frequently.

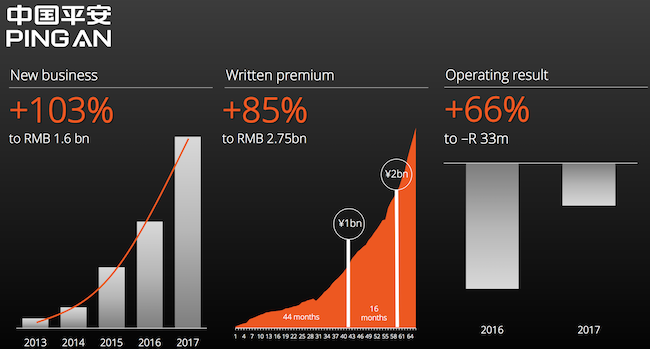

From an investors perspective, the most exciting part of the business is their JV in China. The number of new customers increased by 428% last year to 3.7 million lives, a drop in the ocean for China. The operation is still loss-making but is expected to reach break-even during next year. Adrian emphasised that they are more focused on building a solid foundation than becoming profitable as soon as possible.

Over the last two-years the Discovery share price is flat, but since January they are up 25%. Part of the concern was that Discovery would need to do another rights issue to fund their international growth and the bank that they are launching in South Africa (expected for the second quarter of 2018). As the year has gone on it became increasingly clear that a rights issue was not needed.

The stock is not cheap at a P/E of 21, when earnings only grew 8% last year. Going forward though, they have a long pipeline of strong profit producing businesses. Their 'emerging businesses' will become more established and the Chinese division has the potential to become their most significant profit centre. We back Adrian Gore's vision for the company and their world-leading IP. A buy in our books.