Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

Good news, Famous Brands results for the full year hit the screens yesterday morning. The same cycle over and over, the longer you do this, the more you get used to the fact that the company is going to report on the last Monday in May. These of course were for the full year to end 29 February - Famous Brands Reports Impressive 15th Consecutive Year Of Record Results. It is a pretty impressive track record and most especially against the backdrop of a consumer that was supposed to be under tremendous pressure. They are opening two stores a week here in South Africa, three a week across the group, and they refurbished four stores across the group per week of the financial year.

When you own this business, you are leveraging off their ability to learn from the prior years of experience in manufacturing at scale and their ability to deliver timeously to their franchise owners. In other words, whilst the strength of their front end businesses is paramount and most importantly continuing to attract new (and retain existing) customers, the margin expansion in manufacturing continues to be more important. If you can produce at scale, cheaper product to then on-sell to your franchise owners, that feeds straight through to the bottom line. Franchise owners have strict instructions in order to meet the lofty standards (that counts for all brands), which is why they have to buy everything from buns to serviettes from the company itself. In essence you are buying a logistics (huge network) business that services 2614 restaurants.

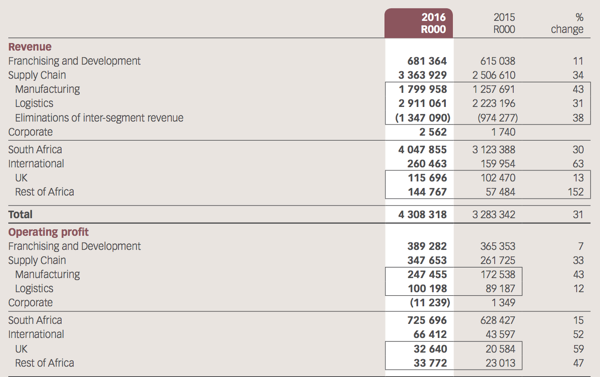

Herewith the divisional revenues and operating profits, equally across the different geographies. See that whilst Franchising and development profits grew only 7 percent, notice that the supply chain division (manufacturing and moving goods around) grew at a whopping 33 percent. Also quite noticeable was that the rest of Africa segment grew at an incredible pace. More importantly for shareholders, it is now bigger than the UK, in terms of revenues and profits. Still, the business is very South African, which isn't necessarily a bad thing:

If you recall last week the manufacturing division was dealt a shot in the arm, Famous Brands bought a french fries processing plant from Oceana. It is called Lamberts Bay Foods and currently processes 24 thousand tons of potatoes per annum. Of course remember that through their franchises such as Steers and Wimpy, the group sells a monster amount of french fries. There are over 600 franchised Wimpy's in South Africa, Steers has a similar number just under 600, there are 227 Fishaways, as you can see, nearly half of their brand presence needs french fries all the time.

The one that rich people talk about all the time is Tasha's, the founder Natasha Sideris still is very much operational. There are only 16 Tasha's, one in Dubai, one in Durban, one in Pretoria, four in Cape Town and the balance, the other half, here in Jozi. One in fact here in Melrose Arch where we are. I have been to 5 I think, including the one here. Yes, five. None outside of Joburg, as of yet. I recall seeing Tasha at the Sandton store, she was at the store on a Saturday morning being highly in tune with the restaurant. Getting staff to make sure presentation was perfect. I remember some plants were not quite up to scratch, there was a little dust on the top of a shelf, that sort of thing. Heck, I guess you don't get to be a highly driven entrepreneur without perfection. I wonder if she retained the 49 percent stake as per the 2008 deal, I guess she may have the finance backing of the banks if Famous Brands is the partner.

I think that is the other part of the model, recently Famous Brands have been looking for more casual dining experiences, fine dining without the pomp and ceremony. That is why they have been acquiring controlling stake in the likes of Salsa Mexican Grill (I have been there too, the single branch in Fourways is awesome), I think that one is going to be a massive hit. Lupa Osteria, the three branch spot in KZN, if any of you have been there, please let me know. Catch, there seems to also only be a single branch (as far as I can tell) in Bedfordview, my friends from the East, have you been there? And of course French bakery concept PAUL will be hitting our shores soon. A school dad will be running that business, I have had the time to chat to him and get insight, equally I have been to their bakery outlets in Paris, pretty darn awesome places.

What I find pretty amusing is that whilst the general rhetoric points to a gloomy outlook, the company suggests that they are opening 292 franchise restaurants this year. How bad can it be? They are adding in the next year over 11 percent to the existing base. Those stores will continue to require a strong manufacturing presence. As they say in the prospects column: "Famous Brands will continue to pursue further upstream manufacturing prospects and explore opportunities to grow the Group's presence in the casual evening dining segment, as well as outside of the traditional food service sector"

Howard Schultz was recently in South Africa for Taste Holding's opening of the Starbucks in Rosebank (I still haven't been), and being there a week after the actual opening, suggested that this market could be really strong in accepting of their brand. We like all the entrants in this space, Taste will have to execute carefully, they have the energetic management to do that, of that I have no doubt. The casual dining market, notwithstanding the current environment, looks in good shape.

As an investment, Famous Brands always looks (perpetually) expensive trading on (at the close yesterday of 121.45 Rand) a 22.5 multiple. Growing at that pace means that the PEG ratio (Price to earnings over the growth in earnings, which is 16 percent over the last 6 years) is 1.4 times. There is a very generous dividend policy of 1.3 times, the dividend for the year clocked 405 cents, after the 15 percent DWT (dividend withholding tax) the yield is 2.83 percent. Not a kings ransom, progressive nevertheless. We continue to own and accumulate the shares on weakness.