Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

US markets closed at another record high yesterday, closing out the best quarter for stocks since December 2023. We expect this positive momentum to continue as earnings season kicks off in a few weeks. Previously, a strong dollar has been a headwind for the tech-titans, but now it will swing to a tailwind for companies that earn a lot of money outside the US, giving a nice boost to profits.

In company news, HP popped 11% after settling a lawsuit with the Department of Justice, clearing the way for it to acquire Juniper Networks, which was also up 8.45%. Elsewhere, Amazon dropped 1.75% after former CEO Jeff Bezos announced he's selling $5.4 billion worth of shares. The amount up for sale is insignificant for him, and it continues his trend of selling a few billion each year. Also, he has to pay for his wedding.

In summary, the JSE All-share closed up 0.59%, the S&P 500 marched 0.63% higher, and the Nasdaq added a fresh 0.52%. That will do nicely, thanks.

In recent months we've been buying shares of Booking Holdings for clients. As you probably know, it's the world's largest online travel agent. Now that Covid is behind us, demand for local and overseas travel is through the roof.

Booking connects users to 31 million accommodation options in over 220 countries, and sells more than 3.5 million room nights every single day. There are also numerous services for car rentals, flights and travel packages. It spends a ton of money on Google, to appear when users search for 'hotels in [insert city name]'.

It's not just a platform for end-users. It has a sophisticated online engine that is used by their hotel partners to flag room availability and update prices.

The business has an interesting backstory. It was founded in 1996 by a Dutchman called Geert-Jan Bruinsma at the University of Twente in Enschede, Netherlands. It was a pan-European operation from the start.

A US-based online travel operator, Priceline, had an ambitious head of mergers and acquisitions called Glenn Fogel (pictured here) who is now the CEO of Booking Holdings. Fogel went on a buying spree, acquiring ActiveHotels.com in 2004 and Booking.com for $133m in 2005. The whole group was renamed Booking in 2018.

Gross bookings are approaching $200 billion per year, and they capture about 10% of that flow as revenue. Both of those metrics are rising at around 10% year-on-year.

This is a good one, you should consider adding some Booking shares to your Vestact portfolio.

We often get asked "what's the best time to buy?" Our standard reply of "when the funds are ready" may sound like a lazy answer, but research shows that steadily averaging into a market that continues to grow is the easiest way to boost your returns.

I really like this picture from Brian Feroldi - just keep buying. Sometimes you buy the dip or sometimes your short-term timing sucks. But as the base grows through consistent additions and share price appreciation, the compounding really starts to take effect.

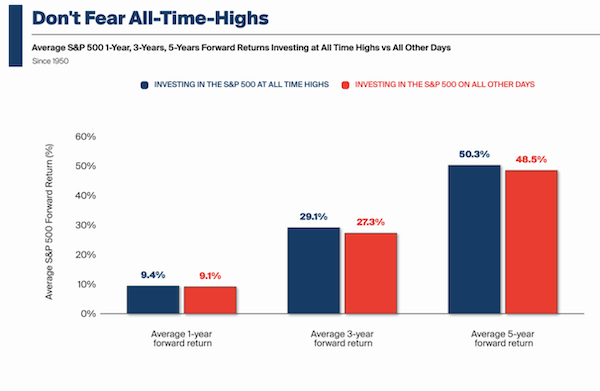

If a stock isn't setting regular all-time highs, why bother buying it? You want to own something that is going up, which is why you shouldn't be afraid to deploy fresh capital at market highs.

US markets hit a new all-time high last week, and Barry Ritholtz wrote the following blog post - All-time highs are bullish.

"The data shows that if you invest during all-time highs, you do better than you would if you're investing randomly on any other day in a market cycle". He analyses prior cycles: "To avoid that very last all-time high, the 479th one before the March 2000 top, you would have had to miss a substantial number of the 478 prior highs that preceded it over the prior 16 years or so. The odds there make that seem like a terrible bet to me".

Don't overthink things. If you have fresh long-term funds available, get stuck into the market.

The new Vera C. Rubin telescope is incredible. It's perched on a mountaintop in the Chilean Andes and observes the whole sky every three days - An astronomical marvel.

Does everything hurt when you get up in the morning? The older you get, the more likely you're going to twist, sprain, or break something in your body - Tips on how not to strain your body.

Asian markets are mixed this morning, mainland China and South Korea are higher, but Japan and Hong Kong are lower. Japanese shares are weaker as Trump threatened to impose fresh tariffs, beefing about them not buying US-grown rice. The two countries are nearing a new trade deal, so this sounds like a bit of manoeuvring to push for extra concessions from Japan.

In local market news, industrial investment company Invicta rose by 4.6% yesterday on their latest numbers. They only grew revenue by 6%, but thanks to the sale of an Asian property, they booked a nice profit and had a cash boost. They used that money to buy back an impressive 6% of the shares in issue.

US futures are flat and the Rand is at $/R17.71 - our currency has been remarkably stable this year.

Have a prosperous day.

We manage USD accounts in New York, with highly-personalised service. We've delivered industry-beating performance, thanks to low fees and good stock-picking.

Click here for more information, or email support@vestact.com.