Sign up for our free daily newsletter

Get the latest news and some fun stuff

in your inbox every day

Get the latest news and some fun stuff

in your inbox every day

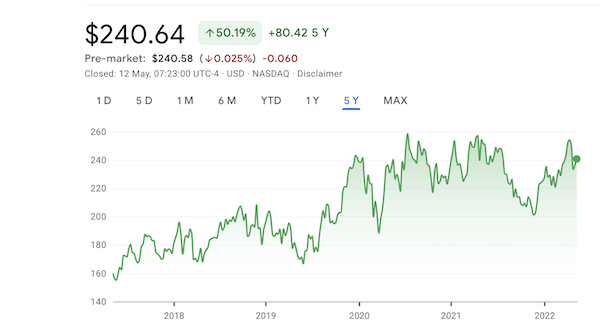

If you owned pharma giant Amgen during 2020 and 2021 you might have felt disappointed as it drifted sideways while everything else went up. But this year, it's actually up 6% while everything else has tanked. Its solid margins, reliable revenues and healthy dividend yield (well above 3% per annum) has meant that Amgen has stood strong when called upon.

Amgen's first-quarter results released at the end of April beat consensus on both revenues and earnings. Sales of their broad range of patented and biosimilar products were pleasing. In layman's terms, biosimilars are the equivalent to generic drugs in the biotech world.

Amgen sells 18 approved and branded drugs that are in various stages of growth and maturity. Out of $6.2 billion in revenue, $5.3 billion is gross profit, which is incredible. But remember they spend $1 billion a quarter on research and development. The expensive part is inventing the product. Manufacturing at scale and then selling it is the easy part.

The Amgen share price has gone sideways for the last two years because they haven't had a blockbuster new launch in a while. The existing business is in good shape though and the dividend pays you while you wait. This one is worth holding until more new products come online.